- Investment Research Partners

- Feb 4

- 4 min read

Updated: Feb 5

Executive Summary

After a strong 2025 calendar year for most asset classes, the new year began on a positive note despite some volatility mid-month.

The rotational trade away from large US technology stocks toward some of the less-loved parts of the market, such as biotechnology, dividend-oriented, and non-US stocks, continued.

The Federal Reserve (Fed) decided to leave interest rates unchanged at its January meeting; however, the more important news was President Trump’s nomination of Kevin Warsh to replace Jerome Powell as Fed Chair when Powell’s term ends in May.

Assuming Warsh is confirmed, it will usher in a new era for the Federal Reserve; however, what that means for the economy and markets remains to be seen.

Market Rotation Persists

January started the new year on a positive note, with most equity markets posting gains despite some volatility. Equity markets retreated briefly mid-month as the threat of tariffs and an escalation in rhetoric over the US taking control of Greenland heightened. While the news initially rattled markets and raised questions about NATO’s future, markets quickly recovered after President Trump announced “the framework for a future deal” at the World Economic Forum in Switzerland.

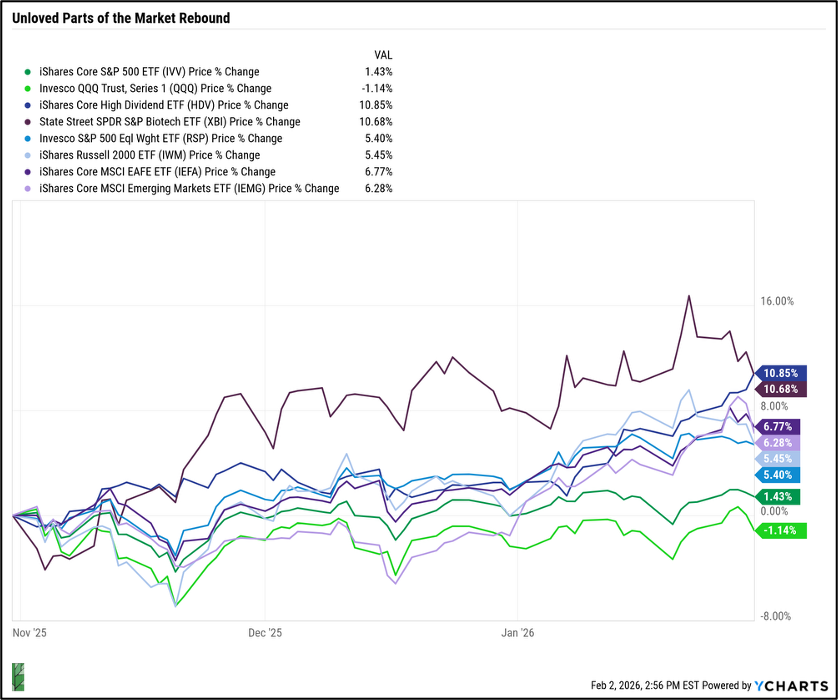

The first month of 2026 continued a trend that first began in the fourth quarter of last year – the rotation in equity market leadership from large US technology stocks to parts of the market that had previously lagged. Dividend payers and biotechnology stocks are up over 10% since November 1, and small-cap, equal-weight, and non-US stocks have all performed relatively well (as represented by the exchange-traded funds below). The S&P 500 and Nasdaq 100 (a proxy for large US technology stocks) have been the laggards over the past three months after leading the past few years (as represented by ETFs in green below).

Many potential theories for this rotation exist; however, none are definitive at this point. Whether we are witnessing concern over AI-related stock valuations or the AI trade is beginning to broaden out to other sectors, we do not know. Regardless, remaining diversified by maintaining exposure to the overlooked and unloved parts of the market has proven beneficial over the past few months.

New Leadership at the Fed

The Federal Reserve met in January and decided to hold the target short-term interest rate steady. After three straight reductions, this marks the first meeting since July of last year that the Fed hasn’t reduced rates. At the post-meeting press conference, Chair Powell stated it is “hard to look at the data and say that policy is significantly restrictive right now.” Worth noting, there were two dissents in favor of reducing rates at this meeting, highlighting the differing opinions among voting members.[1][2]

The bigger Fed-related story came after the meeting, as President Trump announced his nomination of Kevin Warsh as the next Chair, to succeed Jerome Powell, whose term ends in May (although he can continue serving as a Fed governor until 2028). Warsh is a Wall Street veteran who also served on the Federal Reserve’s Board of Governors through the Great Financial Crisis of 2008-2009. By most accounts, Warsh is viewed as a qualified and credible choice as the next Fed Chair.[3] Markets remained relatively calm after the announcement, with neither the stock nor bond markets reacting meaningfully.

Warsh has been openly critical of the Fed since leaving it, however, and he has suggested that reform is needed. For example, he has argued for the Fed’s balance sheet being reduced dramatically and for the Fed Funds rate to be lowered. In addition, he has advocated for reducing staff.

While changes for the Fed may be on the horizon later this year, it is important to note that the Federal Funds target rate is set by the majority of the Federal Open Market Committee. Assuming he is confirmed, Warsh will be just one of 12 voting members. As for the myriad questions the announcement raises – including Fed independence, whether Powell will remain on the FOMC until 2028, and what reforms may come – we see no reason to speculate, as answers will come soon enough.

The Path Forward

This year has begun much as last year played out, with some volatility around potential tariffs and news about the Fed, but markets ultimately grinding higher. We are also currently in a partial government shutdown, also reminiscent of the longest government shutdown on record in October and November of last year (although this one may be brief).[4]

As the environment to begin 2026 looks much like 2025, we continue to advocate for remaining diversified. As circumstances evolve, we will adapt accordingly. We appreciate your continued trust and welcome the opportunity to speak with you in greater detail regarding your specific situation.

[3] Source: https://www.bloomberg.com/news/articles/2026-01-30/kevin-warsh-and-the-fed-will-his-nomination-for-chair-change-monetary-policy?itm_source=record&itm_campaign=The_Fed&itm_content=Kevin_Warsh-0

Important Information

All investments contain risk and may lose value. Past performance is not an indication of future performance. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all clients and each client should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Certain third-party sources cited in this material may require a paid subscription or may otherwise be located behind a paywall. If you would like more information regarding any cited source, please contact IRP and we will provide additional details upon request.

Click below to view our February 2026 Market Outlook video